Initial Filing and Payment for the Global Minimum Tax

Global Minimum Tax is a regime designed to ensure that multinational enterprise (MNE) groups pay a minimum effective tax rate of 15% regardless of the jurisdiction in which they operate. Where the effective tax rate in a particular jurisdiction falls below 15%, the shortfall (top-up tax) may be imposed by the jurisdiction of the parent entity or other relevant jurisdictions.

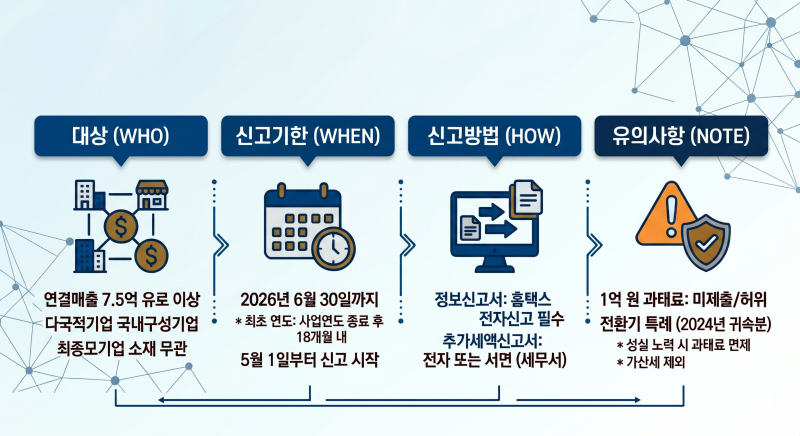

(Entities Subject to Filing and Payment)

Revenue Threshold: Constituent entities of multinational enterprise groups with consolidated revenue of at least EUR 750 million (approximately KRW 1 trillion) in at least two out of the preceding four fiscal years.

Filing Obligation: All Korean constituent entities within an in-scope group are required to file, regardless of the location of the ultimate parent entity or whether the relevant foreign jurisdiction has implemented the rules.

Excluded Entities: Government entities, international organizations, non-profit organizations, pension funds, and certain other excluded entities are outside the scope of the rules.

(Key Filing Deadlines and Methods)

Filing and Payment Deadline: By 30 June 2026 (Tuesday).

However, for the initial year of application, filing may be made by the later of: (i) 18 months after the end of the fiscal year, or (ii) 30 June 2026.

Filing Methods:

GloBE Information Return: Electronic filing through Hometax only.

Top-up Tax Return: May be filed electronically through Hometax or submitted to the tax office by mail or in person.

(Types of Filing Documents)

GloBE Information Return (GIR): The primary filing containing general information on the MNE group and detailed tax calculation information. Filing in Korea may be exempt if a designated local filing entity submits the return on behalf of the group, or if an overseas constituent entity files the return in a jurisdiction with an information exchange agreement.

Overseas Constituent Entity Information Return: Supplemental filing required in Korea where the GIR has been submitted overseas.

Top-up Tax Return: Required where additional top-up tax is payable.

(Penalties and Transitional Relief)

Administrative Penalty: Failure to file, late filing, or submission of false information may result in an administrative penalty of up to KRW 100 million.

Transitional Relief: In recognition of the initial implementation phase, penalties for non-filing or underreporting for the 2024 fiscal year may be waived where taxpayers have made good-faith efforts to comply.

Please also note that the fiscal year for Global Minimum Tax purposes must be aligned with the fiscal year used in the ultimate parent entity’s consolidated financial statements. In addition, the GloBE Information Return should be prepared in the functional currency (foreign currency), while the Top-up Tax Return must be prepared and filed in Korean Won (KRW).

혜성회계법인 뉴스레터는 혜성회계법인의 고객을 위한 일반적인 정보제공 및 지식전달을 위하여 배포되는 것으로, 구체적인 회계문제나 세무이슈 등에 대한 혜성회계법인의 의견을 포함하고 있는 것은 아닙니다. 혜성회계법인의 뉴스레터에 담긴 내용과 관련하여 보다 깊이 있는 이해나 의사결정이 필요한 경우에는, 반드시 관련 전문가의 자문 또는 조언을 받으시기 바랍니다.

Hyesung newsletter has been prepared for the provision of general information and knowledge for clients of Hyesung, and does not include the opinion of Hyesung on any particular accounting or tax issues. If you need further information or discussion concerning the content contained in the Hyesung newsletter, please consult with relevant experts.

ⓒ 2026 Hyesung Accounting Corporation. All rights reserved.

혜성회계법인 | 혜성어드바이저리

www.hscpa.co.kr 서울특별시 강남구 강남대로 308 랜드마크타워 21F (06253)

Tel. 02-516-5434 | E mail. admin@hscpa.co.kr 수신거부Unsubscribe