The season for appointing external auditors for December year-end corporations for 2026 is now in full swing. According to a recent announcement by the Financial Supervisory Service (November 26, 2025), there has been a rapid surge in companies subject to forced auditor designation due to violations of appointment deadlines or procedures. Therefore, extreme caution is required.

HYESUNG has conducted an in-depth analysis of the FSS press release to summarize the key checkpoints you must verify when appointing an auditor for 2026.

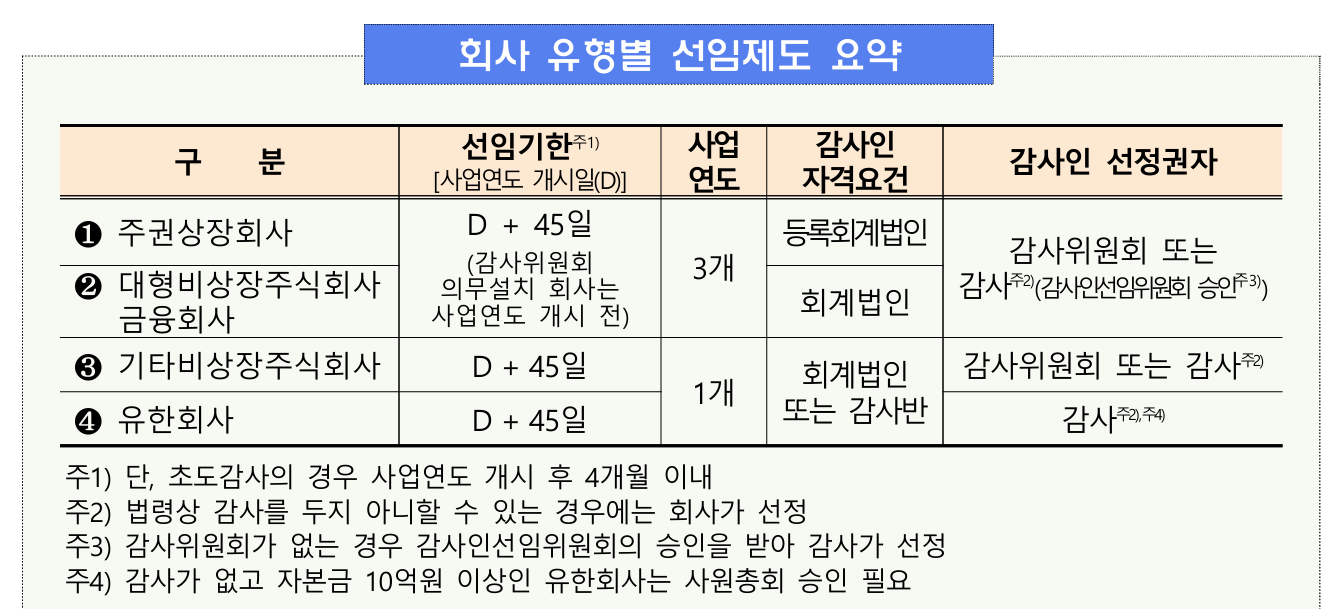

📅 2026 Auditor Appointment Deadlines (For December Year-End Company)

- General Companies (Continuing Audit Targets)

- General listed and unlisted companies not required to establish an Audit Committee.

- Deadline: February 19, 2026 (Thu) (Within 45 days of the start of the fiscal year. However, the deadline has been extended to Feb 19 due to the Lunar New Year holidays, etc.)

- Companies Required to Establish an Audit Committee

- Listed companies with assets of KRW 2 trillion or more, financial companies, etc.

- Deadline: December 31, 2025 (Before the start of the fiscal year)

- Initial Audit Companies

- Companies that did not undergo an external audit in the preceding fiscal year.

- Deadline: April 30, 2026 (Within 4 months of the start of the fiscal year)

🚨 'Critical Mistakes' Leading to Auditor Designation

These are the most frequent violation types pointed out by the FSS. Violating the following may result in the designation of an auditor by the regulator.

- Misunderstanding the Deadline (Continuing vs. Initial Audit): Companies audited last year are targets for "continuing audit" this year. It is a violation if you mistake the deadline for the initial audit deadline (end of April) and miss the February 19 deadline.

- Overlooking Change in Company Type (Unlisted → Large Unlisted): If your company has become a "large unlisted company" due to asset growth, you must re-sign a 3-year contract through the approval of the Auditor Appointment Committee, even if retaining the existing auditor.

- Failure to Change to Registered Accounting Firm After Listing: Even if you contracted with a non-registered accounting firm prior to listing, you must change to a Registered Accounting Firm immediately upon listing.

- Errors in Auditor Appointment Committee Composition: An internal auditor can never be the chairperson. Internal directors or employees cannot be members. An external expert can only serve as a chairperson and cannot participate as a regular member.

- Omission of Auditor Appointment Report: When appointing an auditor through the approval of the Auditor Appointment Committee (Listed companies, Large unlisted companies, etc.), you must file an appointment report every time, even if the auditor has not changed.

✅ Essential Checklist for Practitioners

The Company must verify the following items before proceeding with the appointment process.

- [Type Check] Is our company a listed company, a large unlisted company (Assets ≥ KRW 100bn, etc.), or a financial company?

- [Deadline Check] Is it possible to sign the contract by February 19, 2026 (Thu)?

- [Qualification Check] Does the selected auditor have the qualifications matching our company type (Registered Accounting Firm / Accounting Firm)?

- [Procedure Check] Is the approval procedure for the Audit Committee or Auditor Appointment Committee lawfully planned? (Especially regarding chairperson qualifications)

- [Report Check] Are you preparing the report to the FSS within 2 weeks after signing the contract?

Please refer to the linked pages below for more details.

HYESUNG Accounting Corporation supports your company's stable external auditor appointment process. If you need assistance or advice regarding the review of external audit requirements, appointment procedures, or Auditor Appointment Committee composition, please feel free to contact us at any time.

Contact

Chris Song, Partner | E. cwsong@hscpa.co.kr

Josh Kim, Partner | E. jskim@hscpa.co.kr